金融与信モデル(6)——実例:モデルの構築

金融与信モデル入門シリーズ

- スコアカードの由来

- 証拠の重さと情報価値(WOE and IV)

- グルーピングの方法(Grouping Method)

- 信頼できるAIの要素——PSI(Population Stability Index)

- スコアの計算

- 実例:モデルの構築

ソースコード:GitHub Repository

Tool explanation

Lapras Package Install

via pip

pip install lapras --upgrade -i https://pypi.org/simple

import lapras

import pandas as pd

import numpy as np

from sklearn.model_selection import train_test_split

import matplotlib as mpl

import matplotlib.pyplot as plt

pd.options.display.max_colwidth = 100

import math

%matplotlib inline

from IPython.display import display, HTML

display(HTML("<style>.container { width:90% !important; }</style>"))

from IPython.core.interactiveshell import InteractiveShell

InteractiveShell.ast_node_interactivity = "all"

Read in data file

Note:Data comes from:https://www.kaggle.com/competitions/GiveMeSomeCredit/data

df_training = pd.read_csv('data/cs-training.csv',encoding="utf-8", index_col=0)

df_testing = pd.read_csv('data/cs-test.csv',encoding="utf-8", index_col=0)

to_drop = [] # exclude the features which not being used, eg:id

target = 'SeriousDlqin2yrs' # Y label name

Simple EDA(Exploratory Data Analysis)

lapras.detect(df_training)

| type | size | missing | unique | mean_or_top1 | std_or_top2 | min_or_top3 | 1%_or_top4 | 10%_or_top5 | 50%_or_bottom5 | 75%_or_bottom4 | 90%_or_bottom3 | 99%_or_bottom2 | max_or_bottom1 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| int64 | 150000 | 0 | 2 | 0.06684 | 0.249746 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 |

| float64 | 150000 | 0 | 125728 | 6.04844 | 249.755 | 0 | 0 | 0.00296898 | 0.154181 | 0.559046 | 0.981278 | 1.09296 | 50708 |

| int64 | 150000 | 0 | 86 | 52.2952 | 14.7719 | 0 | 24 | 33 | 52 | 63 | 72 | 87 | 109 |

| int64 | 150000 | 0 | 16 | 0.421033 | 4.19278 | 0 | 0 | 0 | 0 | 0 | 1 | 4 | 98 |

| float64 | 150000 | 0 | 114194 | 353.005 | 2037.82 | 0 | 0 | 0.030874 | 0.366508 | 0.868254 | 1267 | 4979.04 | 329664 |

| float64 | 150000 | 0.1982 | 13594 | 6670.22 | 14384.7 | 0 | 0 | 2005 | 5400 | 8249 | 11666 | 25000 | 3.00875e+06 |

| int64 | 150000 | 0 | 58 | 8.45276 | 5.14595 | 0 | 0 | 3 | 8 | 11 | 15 | 24 | 58 |

| int64 | 150000 | 0 | 19 | 0.265973 | 4.1693 | 0 | 0 | 0 | 0 | 0 | 0 | 3 | 98 |

| int64 | 150000 | 0 | 28 | 1.01824 | 1.12977 | 0 | 0 | 0 | 1 | 2 | 2 | 4 | 54 |

| int64 | 150000 | 0 | 13 | 0.240387 | 4.15518 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 98 |

| float64 | 150000 | 0.0262 | 13 | 0.757222 | 1.11509 | 0 | 0 | 0 | 0 | 1 | 2 | 4 | 20 |

Calculate IV value of features(Calculate by default decision tree binning)

lapras.quality(df_training.drop(to_drop,axis=1),target = target)

| iv | unique |

|---|---|

| 1.16303 | 125728 |

| 0.880725 | 19 |

| 0.761485 | 16 |

| 0.601348 | 13 |

| 0.264446 | 86 |

| 0.111157 | 58 |

| 0.093006 | 13595 |

| 0.077739 | 114194 |

| 0.065721 | 28 |

| 0.036456 | 14 |

Calculate PSI of features between train and test dataset

All the PSIs are very small, that says the populations are stable.

cols = list(lapras.quality(df_training,target = target).reset_index()['index'])

for col in cols:

if col not in [target]:

print("%s: %.4f" % (col,lapras.PSI(df_training[col], df_testing[col])))

D:\anaconda3\lib\site-packages\lapras\stats.py:191: FutureWarning: iteritems is deprecated and will be removed in a future version. Use .items instead.

RevolvingUtilizationOfUnsecuredLines: 0.0001

NumberOfTimes90DaysLate: 0.0000

NumberOfTime30-59DaysPastDueNotWorse: 0.0000

NumberOfTime60-89DaysPastDueNotWorse: 0.0000

age: 0.0001

NumberOfOpenCreditLinesAndLoans: 0.0001

MonthlyIncome: 0.0005

DebtRatio: 0.0001

NumberRealEstateLoansOrLines: 0.0001

NumberOfDependents: 0.0001

Calculate VIF

There are some multi-correlations in the dataset.

lapras.VIF(df_training.drop(to_drop,axis=1))

lapras.VIF(df_testing.drop(to_drop,axis=1))

SeriousDlqin2yrs 1.033037

RevolvingUtilizationOfUnsecuredLines 1.000180

age 0.271682

NumberOfTime30-59DaysPastDueNotWorse 41.465993

DebtRatio 1.027033

MonthlyIncome 1.026314

NumberOfOpenCreditLinesAndLoans 1.231288

NumberOfTimes90DaysLate 73.738360

NumberRealEstateLoansOrLines 1.255707

NumberOfTime60-89DaysPastDueNotWorse 93.546744

NumberOfDependents 1.030817

dtype: float64

SeriousDlqin2yrs 0.000000

RevolvingUtilizationOfUnsecuredLines 1.000302

age 1.042585

NumberOfTime30-59DaysPastDueNotWorse 46.935924

DebtRatio 1.025020

MonthlyIncome 1.005398

NumberOfOpenCreditLinesAndLoans 1.286748

NumberOfTimes90DaysLate 88.667497

NumberRealEstateLoansOrLines 1.252250

NumberOfTime60-89DaysPastDueNotWorse 112.127576

NumberOfDependents 1.028935

dtype: float64

Dividing the training set into training and validating set

train_df, val_df, _, _ = train_test_split(df_training, df_training[[target]], test_size=0.2, random_state=42)

test_df = df_testing

Features selection

Automatically selecting features by IV, missing rate, corelations and VIF

train_selected, dropped = lapras.select(train_df.drop(to_drop,axis=1),target = target, empty = 0.95, \

iv = 0.05, corr = 0.9, vif = False, return_drop=True, exclude=[])

print(dropped)

print(train_selected.shape)

train_selected.head(10)

{'empty': array([], dtype=float64), 'iv': array(['NumberOfDependents'], dtype=object), 'corr': array(['NumberOfTime60-89DaysPastDueNotWorse',

'NumberOfTime30-59DaysPastDueNotWorse'], dtype=object)}

(120000, 8)

| SeriousDlqin2yrs | RevolvingUtilizationOfUnsecuredLines | age | DebtRatio | MonthlyIncome | NumberOfOpenCreditLinesAndLoans | NumberOfTimes90DaysLate | NumberRealEstateLoansOrLines |

|---|---|---|---|---|---|---|---|

| 0 | 0 | 29 | 0.0115128 | 4342 | 5 | 0 | 0 |

| 0 | 0.595526 | 55 | 0.835333 | 1833 | 11 | 0 | 1 |

| 0 | 0 | 43 | 0.0434365 | 4166 | 2 | 0 | 0 |

| 0 | 0.39198 | 40 | 0.0597711 | 9000 | 2 | 0 | 0 |

| 0 | 0 | 35 | 0.133598 | 5800 | 12 | 0 | 1 |

| 0 | 0.442956 | 61 | 0.65852 | 7200 | 12 | 0 | 2 |

| 1 | 0.336976 | 27 | 0.275494 | 4500 | 9 | 0 | 0 |

| 0 | 0 | 49 | 0.230708 | 2500 | 5 | 0 | 0 |

| 0 | 0.322778 | 69 | 2754 | nan | 17 | 0 | 1 |

| 0 | 0.133706 | 57 | 0.122251 | 3500 | 7 | 0 | 0 |

Feature Binning

Following methods are supported: monotonous binning,decision tree binning, equal frequency binning,equal step size binning.

You can also adjust binnings by load the json.

c = lapras.Combiner()

c.fit(train_selected, y = target,method = 'dt', min_samples = 0.05,n_bins=8) #empty_separate = False

# c.load({'RevolvingUtilizationOfUnsecuredLines': [0.0001,

# 0.1318,

# 0.3009,

# 0.3963,

# 0.5003,

# 0.6987,

# 0.941],

# 'age': [35.5, 43.5, 52.5, 55.5, 59.5, 63.5, 67.5],

# 'DebtRatio': [0.0193, 0.1368, 0.4164, 0.5055, 0.7714, 2.9942, 995.5],

# 'MonthlyIncome': [930.0, 2000.5, 2649.5, 3456.5, 4833.5, 6596.5, 9930.5],

# 'NumberOfOpenCreditLinesAndLoans': [2.5, 3.5, 5.5, 7.5, 8.5, 13.5, 16.5],

# 'NumberOfTimes90DaysLate': [0.5],

# 'NumberRealEstateLoansOrLines': [0.5, 1.5, 2.5]})

c.export()

<lapras.transform.Combiner at 0x2745de778e0>

{'RevolvingUtilizationOfUnsecuredLines': [0.0001,

0.1318,

0.3009,

0.3963,

0.5003,

0.6987,

0.941],

'age': [35.5, 43.5, 52.5, 55.5, 59.5, 63.5, 67.5],

'DebtRatio': [0.0193, 0.1368, 0.4164, 0.5055, 0.7714, 2.9942, 995.5],

'MonthlyIncome': [930.0, 2000.5, 2649.5, 3456.5, 4833.5, 6596.5, 9930.5],

'NumberOfOpenCreditLinesAndLoans': [2.5, 3.5, 5.5, 7.5, 8.5, 13.5, 16.5],

'NumberOfTimes90DaysLate': [0.5],

'NumberRealEstateLoansOrLines': [0.5, 1.5, 2.5]}

c.transform(train_selected, labels=True).iloc[0:10,:]

| SeriousDlqin2yrs | RevolvingUtilizationOfUnsecuredLines | age | DebtRatio | MonthlyIncome | NumberOfOpenCreditLinesAndLoans | NumberOfTimes90DaysLate | NumberRealEstateLoansOrLines |

|---|---|---|---|---|---|---|---|

| 0 | 00.[-inf,0.0001) | 00.[-inf,35.5) | 00.[-inf,0.0193) | 04.[3456.5,4833.5) | 02.[3.5,5.5) | 00.[-inf,0.5) | 00.[-inf,0.5) |

| 0 | 05.[0.5003,0.6987) | 03.[52.5,55.5) | 05.[0.7714,2.9942) | 01.[930.0,2000.5) | 05.[8.5,13.5) | 00.[-inf,0.5) | 01.[0.5,1.5) |

| 0 | 00.[-inf,0.0001) | 01.[35.5,43.5) | 01.[0.0193,0.1368) | 04.[3456.5,4833.5) | 00.[-inf,2.5) | 00.[-inf,0.5) | 00.[-inf,0.5) |

| 0 | 03.[0.3009,0.3963) | 01.[35.5,43.5) | 01.[0.0193,0.1368) | 06.[6596.5,9930.5) | 00.[-inf,2.5) | 00.[-inf,0.5) | 00.[-inf,0.5) |

| 0 | 00.[-inf,0.0001) | 00.[-inf,35.5) | 01.[0.0193,0.1368) | 05.[4833.5,6596.5) | 05.[8.5,13.5) | 00.[-inf,0.5) | 01.[0.5,1.5) |

| 0 | 04.[0.3963,0.5003) | 05.[59.5,63.5) | 04.[0.5055,0.7714) | 06.[6596.5,9930.5) | 05.[8.5,13.5) | 00.[-inf,0.5) | 02.[1.5,2.5) |

| 1 | 03.[0.3009,0.3963) | 00.[-inf,35.5) | 02.[0.1368,0.4164) | 04.[3456.5,4833.5) | 05.[8.5,13.5) | 00.[-inf,0.5) | 00.[-inf,0.5) |

| 0 | 00.[-inf,0.0001) | 02.[43.5,52.5) | 02.[0.1368,0.4164) | 02.[2000.5,2649.5) | 02.[3.5,5.5) | 00.[-inf,0.5) | 00.[-inf,0.5) |

| 0 | 03.[0.3009,0.3963) | 07.[67.5,inf) | 07.[995.5,inf) | 00.[-inf,930.0) | 07.[16.5,inf) | 00.[-inf,0.5) | 01.[0.5,1.5) |

| 0 | 02.[0.1318,0.3009) | 04.[55.5,59.5) | 01.[0.0193,0.1368) | 04.[3456.5,4833.5) | 03.[5.5,7.5) | 00.[-inf,0.5) | 00.[-inf,0.5) |

cols = list(lapras.quality(train_selected,target = target).reset_index()['index'])

for col in cols:

if col != target:

print(lapras.bin_stats(c.transform(train_selected[[col, target]], labels=True), col=col, target=target))

lapras.bin_plot(c.transform(train_selected[[col,target]], labels=True), col=col, target=target)

for name, series in frame.iteritems():

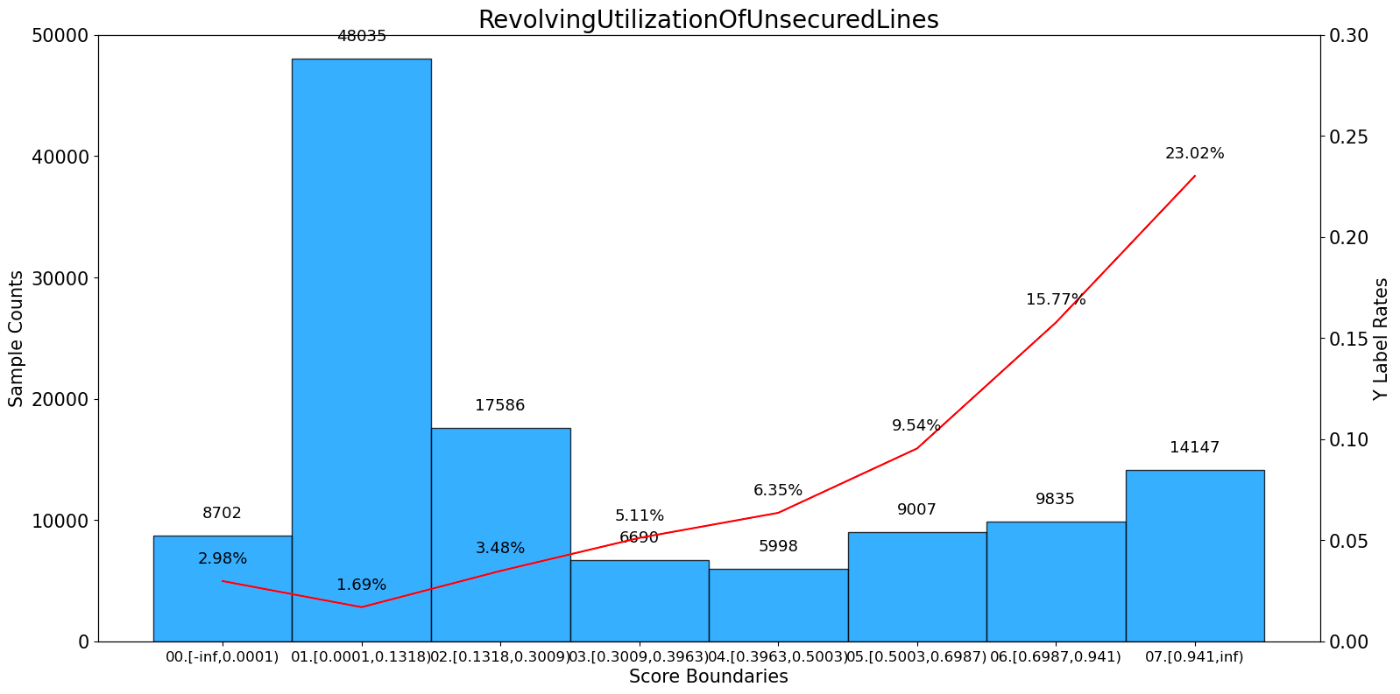

RevolvingUtilizationOfUnsecuredLines bad_count total_count bad_rate \

0 00.[-inf,0.0001) 259 8702 0.029763

1 01.[0.0001,0.1318) 810 48035 0.016863

2 02.[0.1318,0.3009) 612 17586 0.034800

3 03.[0.3009,0.3963) 342 6690 0.051121

4 04.[0.3963,0.5003) 381 5998 0.063521

5 05.[0.5003,0.6987) 859 9007 0.095370

6 06.[0.6987,0.941) 1551 9835 0.157702

7 07.[0.941,inf) 3256 14147 0.230155

ratio woe iv total_iv

0 0.072517 -0.854545 0.037033 1.116664

1 0.400292 -1.435924 0.461712 1.116664

2 0.146550 -0.692986 0.052537 1.116664

3 0.055750 -0.291364 0.004177 1.116664

4 0.049983 -0.061033 0.000181 1.116664

5 0.075058 0.379961 0.012785 1.116664

6 0.081958 0.954294 0.112781 1.116664

7 0.117892 1.422283 0.435457 1.116664

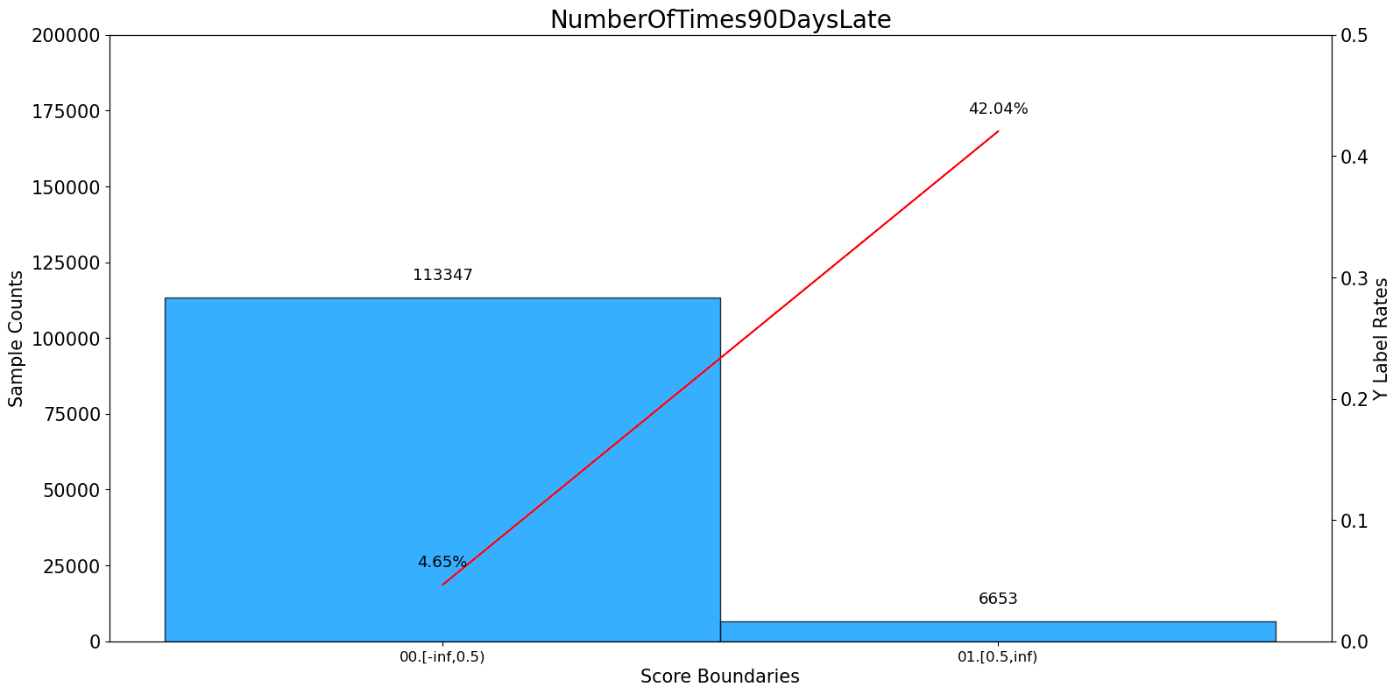

NumberOfTimes90DaysLate bad_count total_count bad_rate ratio \

0 00.[-inf,0.5) 5273 113347 0.046521 0.944558

1 01.[0.5,inf) 2797 6653 0.420412 0.055442

woe iv total_iv

0 -0.390497 0.121890 0.842514

1 2.308637 0.720623 0.842514

age bad_count total_count bad_rate ratio woe \

0 00.[-inf,35.5) 1945 17216 0.112976 0.143467 0.569027

1 01.[35.5,43.5) 1696 18470 0.091825 0.153917 0.338163

2 02.[43.5,52.5) 2071 26274 0.078823 0.218950 0.171275

3 03.[52.5,55.5) 582 8500 0.068471 0.070833 0.019297

4 04.[55.5,59.5) 570 10950 0.052055 0.091250 -0.272280

5 05.[59.5,63.5) 502 11233 0.044690 0.093608 -0.432572

6 06.[63.5,67.5) 278 8547 0.032526 0.071225 -0.762928

7 07.[67.5,inf) 426 18810 0.022648 0.156750 -1.135076

iv total_iv

0 0.059510 0.264022

1 0.020391 0.264022

2 0.006919 0.264022

3 0.000027 0.264022

4 0.006019 0.264022

5 0.014563 0.264022

6 0.030081 0.264022

7 0.126513 0.264022

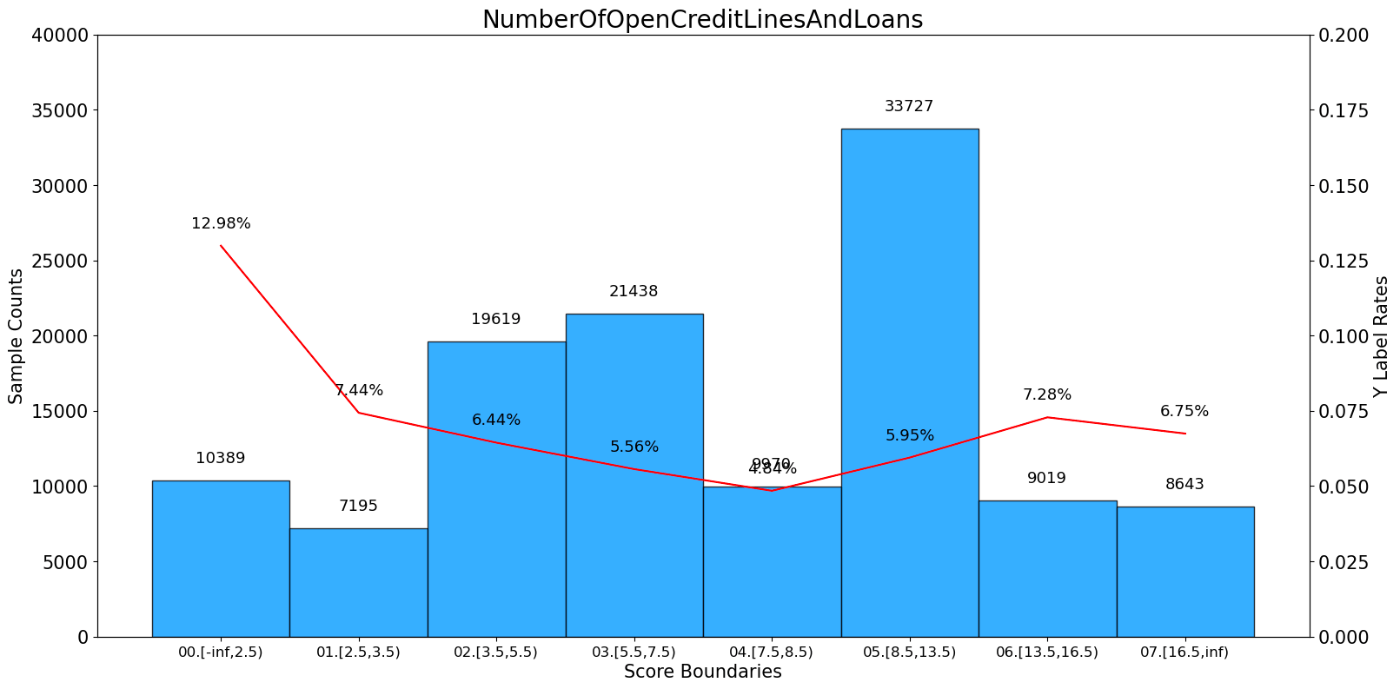

NumberOfOpenCreditLinesAndLoans bad_count total_count bad_rate ratio \

0 00.[-inf,2.5) 1349 10389 0.129849 0.086575

1 01.[2.5,3.5) 535 7195 0.074357 0.059958

2 02.[3.5,5.5) 1264 19619 0.064427 0.163492

3 03.[5.5,7.5) 1193 21438 0.055649 0.178650

4 04.[7.5,8.5) 483 9970 0.048445 0.083083

5 05.[8.5,13.5) 2006 33727 0.059478 0.281058

6 06.[13.5,16.5) 657 9019 0.072846 0.075158

7 07.[16.5,inf) 583 8643 0.067453 0.072025

woe iv total_iv

0 0.727425 6.284771e-02 0.084394

1 0.108112 7.344542e-04 0.084394

2 -0.045901 3.376869e-04 0.084394

3 -0.201717 6.664814e-03 0.084394

4 -0.347941 8.666174e-03 0.084394

5 -0.131116 4.566165e-03 0.084394

6 0.085951 5.763235e-04 0.084394

7 0.003239 7.564700e-07 0.084394

MonthlyIncome bad_count total_count bad_rate ratio woe \

0 00.[-inf,930.0) 1498 27129 0.055218 0.226075 -0.209951

1 01.[930.0,2000.5) 653 6189 0.105510 0.051575 0.492270

2 02.[2000.5,2649.5) 553 6006 0.092075 0.050050 0.341157

3 03.[2649.5,3456.5) 898 8973 0.100078 0.074775 0.433362

4 04.[3456.5,4833.5) 1406 16952 0.082940 0.141267 0.226666

5 05.[4833.5,6596.5) 1246 18452 0.067527 0.153767 0.004400

6 06.[6596.5,9930.5) 1117 20329 0.054946 0.169408 -0.215168

7 07.[9930.5,inf) 699 15970 0.043770 0.133083 -0.454340

iv total_iv

0 0.009105 0.086102

1 0.015486 0.086102

2 0.006757 0.086102

3 0.016959 0.086102

4 0.008009 0.086102

5 0.000003 0.086102

6 0.007150 0.086102

7 0.022634 0.086102

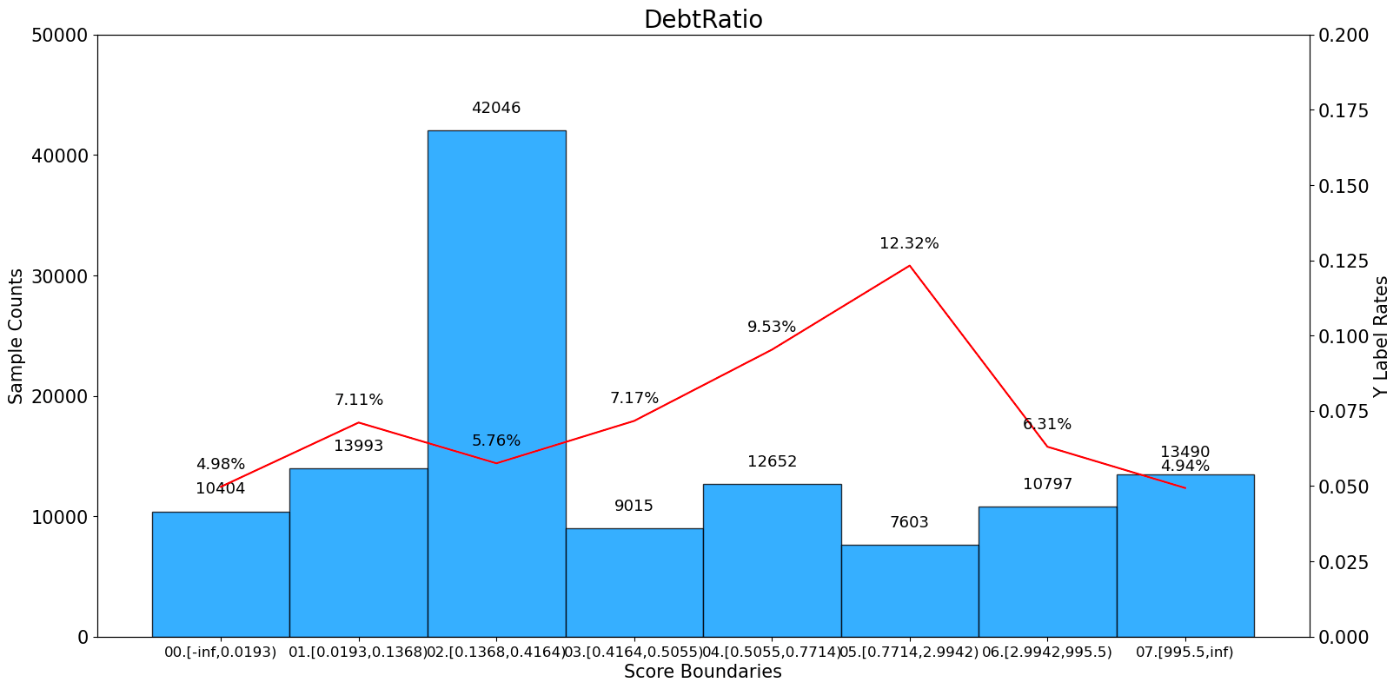

DebtRatio bad_count total_count bad_rate ratio woe \

0 00.[-inf,0.0193) 518 10404 0.049789 0.086700 -0.319179

1 01.[0.0193,0.1368) 995 13993 0.071107 0.116608 0.059912

2 02.[0.1368,0.4164) 2421 42046 0.057580 0.350383 -0.165559

3 03.[0.4164,0.5055) 646 9015 0.071658 0.075125 0.068230

4 04.[0.5055,0.7714) 1206 12652 0.095321 0.105433 0.379389

5 05.[0.7714,2.9942) 937 7603 0.123241 0.063358 0.667628

6 06.[2.9942,995.5) 681 10797 0.063073 0.089975 -0.068591

7 07.[995.5,inf) 666 13490 0.049370 0.112417 -0.328064

iv total_iv

0 0.007703 0.084017

1 0.000430 0.084017

2 0.008943 0.084017

3 0.000360 0.084017

4 0.017900 0.084017

5 0.037757 0.084017

6 0.000411 0.084017

7 0.010512 0.084017

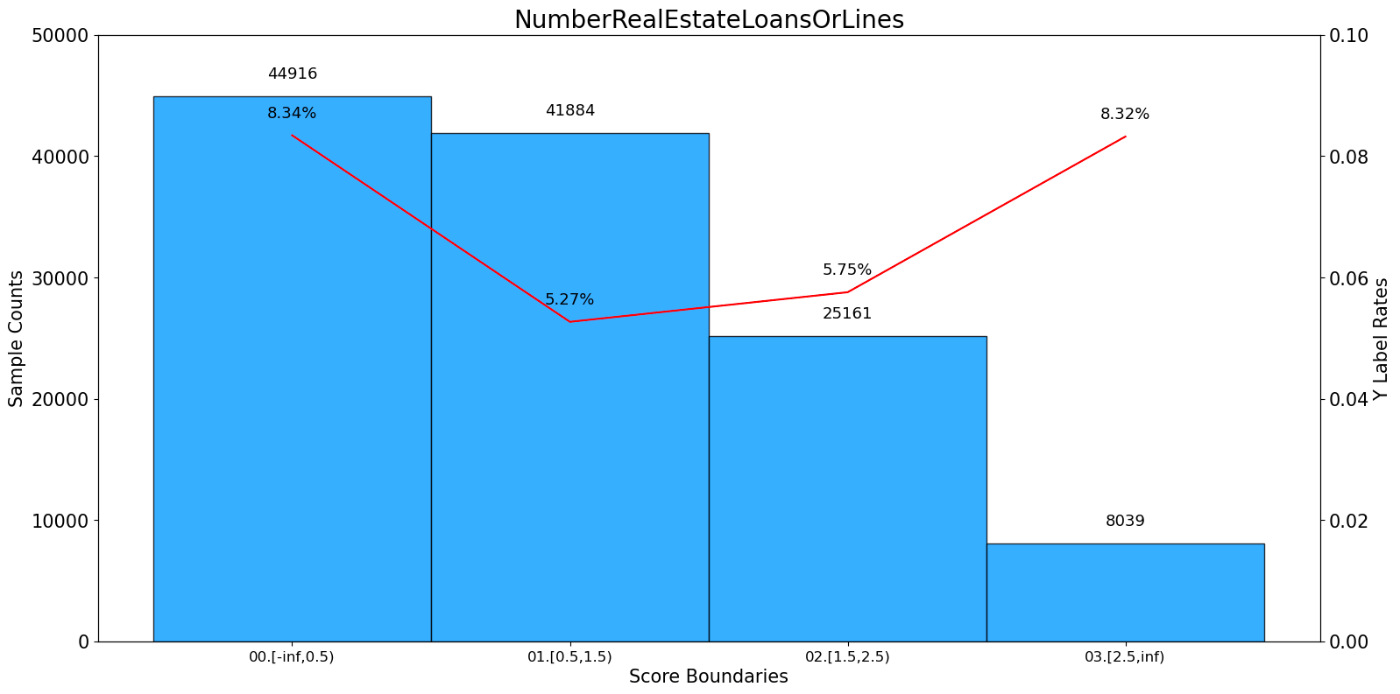

NumberRealEstateLoansOrLines bad_count total_count bad_rate ratio \

0 00.[-inf,0.5) 3747 44916 0.083422 0.374300

1 01.[0.5,1.5) 2206 41884 0.052669 0.349033

2 02.[1.5,2.5) 1448 25161 0.057549 0.209675

3 03.[2.5,inf) 669 8039 0.083219 0.066992

woe iv total_iv

0 0.232990 0.022484 0.052885

1 -0.259896 0.021086 0.052885

2 -0.166120 0.005387 0.052885

3 0.230331 0.003928 0.052885

WOE value transformation

transfer = lapras.WOETransformer()

transfer.fit(c.transform(train_selected), train_selected[target], exclude=[target])

train_woe = transfer.transform(c.transform(train_selected))

val_woe = transfer.transform(c.transform(val_df))

test_woe = transfer.transform(c.transform(test_df))

transfer.export()

<lapras.transform.WOETransformer at 0x2746667ccd0>

{'RevolvingUtilizationOfUnsecuredLines': {0: -0.8545447193506434,

1: -1.435924251083907,

2: -0.6929855643979773,

3: -0.29136415096437573,

4: -0.06103342378641303,

5: 0.37996133825687756,

6: 0.9542941342803827,

7: 1.422282881666063},

'age': {0: 0.5690265657186839,

1: 0.3381626624268103,

2: 0.17127518361124283,

3: 0.01929671368468067,

4: -0.27227960227196496,

5: -0.4325717146160795,

6: -0.7629275544122108,

7: -1.135076460199848},

'DebtRatio': {0: -0.3191794579881027,

1: 0.05991215232361727,

2: -0.16555936062220464,

3: 0.06823001536904652,

4: 0.37938896793740196,

5: 0.6676282169900559,

6: -0.06859110802102461,

7: -0.328063830129681},

'MonthlyIncome': {0: -0.20995147767771272,

1: 0.4922698255982443,

2: 0.341157000215592,

3: 0.4333621138306611,

4: 0.22666561619976386,

5: 0.004400453785423839,

6: -0.21516837009619558,

7: -0.45433994810005246},

'NumberOfOpenCreditLinesAndLoans': {0: 0.7274245964408524,

1: 0.10811217698089041,

2: -0.045900527604813335,

3: -0.20171651274902666,

4: -0.34794087212098535,

5: -0.13111603896185353,

6: 0.08595130018741898,

7: 0.0032385444691370685},

'NumberOfTimes90DaysLate': {0: -0.39049652350955594, 1: 2.308637231090842},

'NumberRealEstateLoansOrLines': {0: 0.23299016747526333,

1: -0.25989576346995086,

2: -0.16611993338112926,

3: 0.23033126856416491}}

IF you want to ensure all the regression params are positive, you can select the features(WOE) once more.

# # Features filtering could be done once more after transformed into WOE value. This is optional.

# train_woe, dropped = lapras.select(train_woe,target = target, empty = 0.9, \

# iv = 0.02, corr = 0.9, vif = False, return_drop=True, exclude=[])

# print(dropped)

# print(train_woe.shape)

# train_woe.head(10)

Stepwise regression, to select best features, this is optional

# final_data = lapras.stepwise(train_woe,target = target, estimator='ols', direction = 'both', criterion = 'aic', exclude = [])

final_data = train_woe

Scorecard modeling

card = lapras.ScoreCard(

combiner = c,

transfer = transfer,

pdo = 40,

rate = 2,

base_odds = 1/60,

base_score = 600

)

col = list(final_data.drop([target],axis=1).columns)

card.fit(final_data[col], final_data[target])

ScoreCard(combiner=<lapras.transform.Combiner object at 0x7e03f8aa9fc0>,

transfer=<lapras.transform.WOETransformer object at 0x7e03effe75b0>)

card.get_params()['combiner']

card.get_params()['transfer']

print("card.intercept_:%s" % (card.intercept_))

print("card.coef_:%s" % (card.coef_))

card.export()

<lapras.transform.Combiner at 0x2745de778e0>

<lapras.transform.WOETransformer at 0x2746667ccd0>

card.intercept_:-2.620820761531965

card.coef_:[ 0.74975573 0.43247525 0.85266412 0.09651427 -0.30244651 0.72712492

0.40350345]

{'intercept': {'[-inf,inf)': 514.97},

'RevolvingUtilizationOfUnsecuredLines': {'[-inf,0.0001)': 36.97,

'[0.0001,0.1318)': 62.13,

'[0.1318,0.3009)': 29.98,

'[0.3009,0.3963)': 12.61,

'[0.3963,0.5003)': 2.64,

'[0.5003,0.6987)': -16.44,

'[0.6987,0.941)': -41.29,

'[0.941,inf)': -61.54},

'age': {'[-inf,35.5)': -14.2,

'[35.5,43.5)': -8.44,

'[43.5,52.5)': -4.27,

'[52.5,55.5)': -0.48,

'[55.5,59.5)': 6.8,

'[59.5,63.5)': 10.8,

'[63.5,67.5)': 19.04,

'[67.5,inf)': 28.33},

'DebtRatio': {'[-inf,0.0193)': 15.71,

'[0.0193,0.1368)': -2.95,

'[0.1368,0.4164)': 8.15,

'[0.4164,0.5055)': -3.36,

'[0.5055,0.7714)': -18.67,

'[0.7714,2.9942)': -32.85,

'[2.9942,995.5)': 3.38,

'[995.5,inf)': 16.14},

'MonthlyIncome': {'[-inf,930.0)': 1.17,

'[930.0,2000.5)': -2.74,

'[2000.5,2649.5)': -1.9,

'[2649.5,3456.5)': -2.41,

'[3456.5,4833.5)': -1.26,

'[4833.5,6596.5)': -0.02,

'[6596.5,9930.5)': 1.2,

'[9930.5,inf)': 2.53},

'NumberOfOpenCreditLinesAndLoans': {'[-inf,2.5)': 12.7,

'[2.5,3.5)': 1.89,

'[3.5,5.5)': -0.8,

'[5.5,7.5)': -3.52,

'[7.5,8.5)': -6.07,

'[8.5,13.5)': -2.29,

'[13.5,16.5)': 1.5,

'[16.5,inf)': 0.06},

'NumberOfTimes90DaysLate': {'[-inf,0.5)': 16.39, '[0.5,inf)': -96.87},

'NumberRealEstateLoansOrLines': {'[-inf,0.5)': -5.43,

'[0.5,1.5)': 6.05,

'[1.5,2.5)': 3.87,

'[2.5,inf)': -5.36}}

train_result = final_data[[target]].copy()

train_result['score'] = card.predict(final_data[col])

train_result['prob'] = card.predict_prob(final_data[col])

val_result = val_woe[[target]].copy()

val_result['score'] = card.predict(val_woe[col])

val_result['prob'] = card.predict_prob(val_woe[col])

test_result = df_testing

test_result['score'] = card.predict(test_woe[col])

test_result['prob'] = card.predict_prob(test_woe[col])

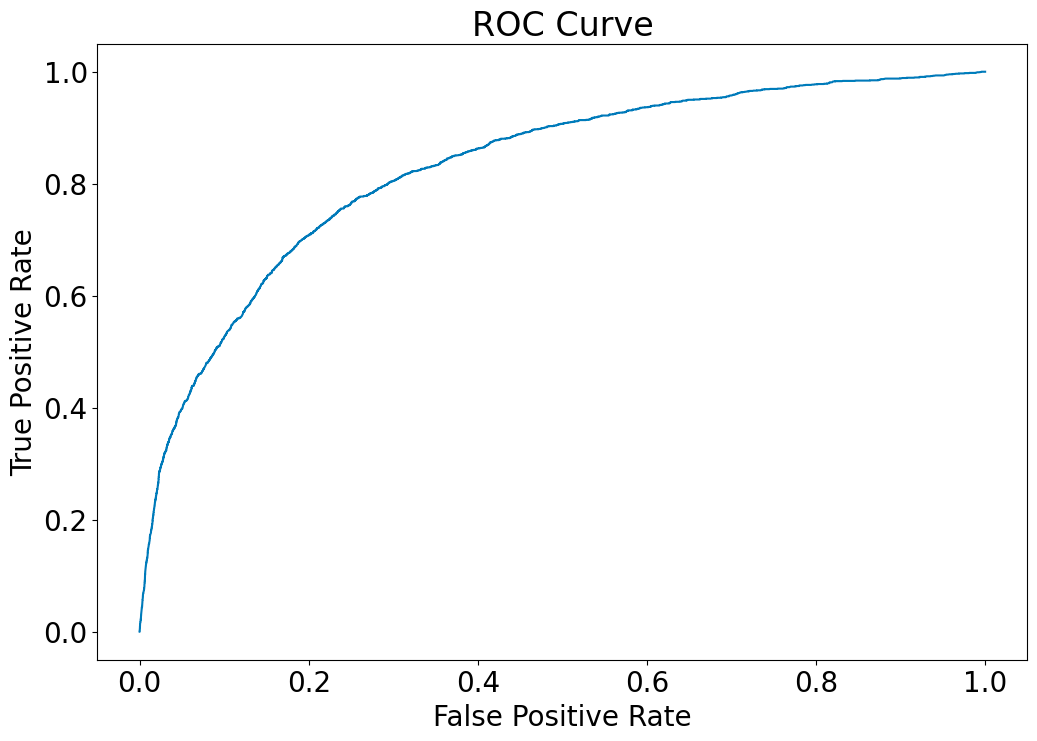

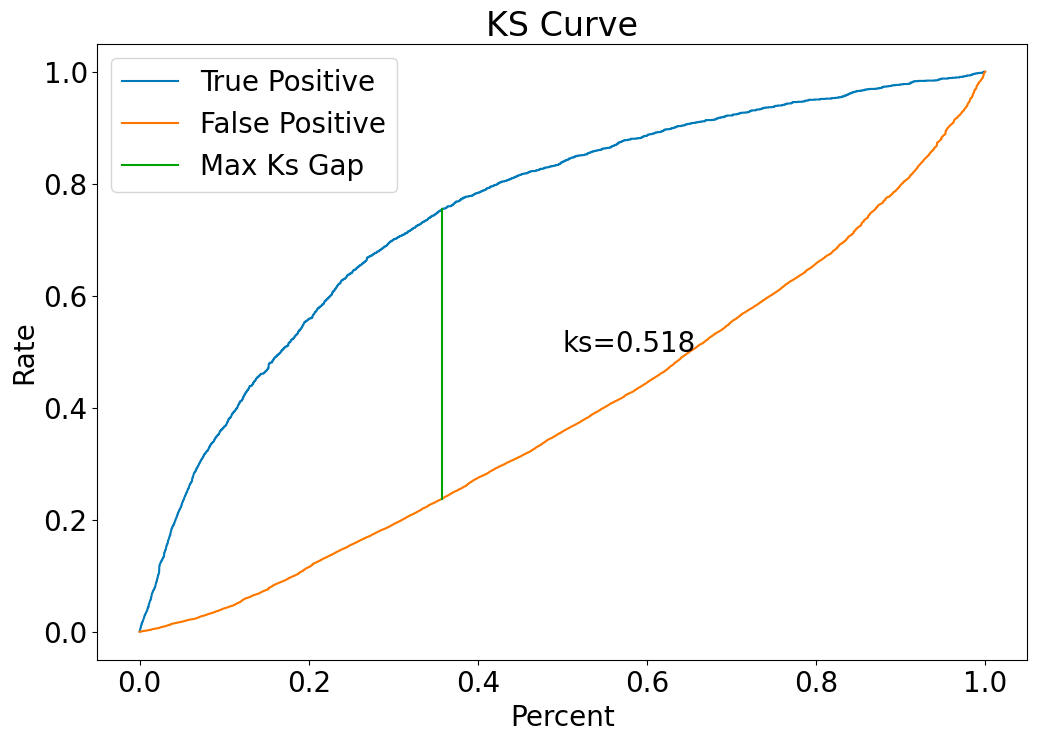

Model performance of validation dataset

lapras.perform(val_result['prob'],val_result[target])

KS: 0.5175

AUC: 0.8289

lapras.score_plot(val_result,score='score', target=target)

lapras.LIFT(val_result['prob'],val_result[target])

| recall | precision | improve |

|---|---|---|

| 0.1 | 0.525469 | 8.05934 |

| 0.2 | 0.475669 | 7.29554 |

| 0.3 | 0.445034 | 6.82568 |

| 0.4 | 0.354649 | 5.43939 |

| 0.5 | 0.282496 | 4.33276 |

| 0.6 | 0.234519 | 3.59691 |

| 0.7 | 0.202575 | 3.10697 |

| 0.8 | 0.159824 | 2.45129 |

| 0.9 | 0.115828 | 1.7765 |

| 1 | 0.0652 | 1 |

Prediction result for test dataset.

test_result[['score','prob']].head(10)

| score | prob |

|---|---|

| 483.52 | 0.111464 |

| 519.46 | 0.0630556 |

| 585.35 | 0.021033 |

| 517.98 | 0.0645845 |

| 445.18 | 0.196006 |

| 526.37 | 0.0563404 |

| 521.72 | 0.0607733 |

| 627.52 | 0.0102394 |

| 644.37 | 0.00766631 |

| 366.5 | 0.487975 |

データサイエンス君のAI教材シリーズ(未経験OK)

教材のターゲット層:

- 初心者: Pythonとデータ分析の基本を学びたい人

- 中級者: より高度な分析手法や機械学習を習得したい人

- レコメンド(推薦)エンジニア: レコメンデーションエンジンを作り、キャリアアップを目指したい人

AI領域に携わりたい方はぜひ!

datasciencekunのAI教材シリーズ

LINE公式アカウント

データサイエンス君のLINE公式アカウント友達募集中!

今登録すれば、下記の内容をプレゼントします!

- 特典資料:AI教材の一部を無料でお送りします!

- 専門家との相談:メッセージでデータサイエンス領域の不明点が相談できます!

一人で学ぶより、仲間と一緒に成長しませんか?

今すぐ友達登録して、データサイエンスの旅を始めましょう!

LINE公式アカウント:https://line.me/R/ti/p/@datasciencekun?from=page&accountId=datasciencekun

Discussion