InformerとAlpha Vantage APIを用いた株価予測メモ

InformerとAlpha Vantage APIを用いた株価予測

ChatGPTで採用されているアルゴリズム、Transformerを改良したInformerアルゴリズムを用いて時系列データである株価予測を行った備忘録

これを使って大損しても責任負いません!

本記事で記述するコードはInformer論文のファーストオーサーであるHaoyi Zhou氏が公開しているGithub Repositoryをアレンジしたものです

Informerとは

AAAI2021 Best paperとなった論文

TransformerのSelf-attentionメカニズムを確率的なスパース化を利用したProbSparse self-attentionメカニズムとしたことで、計算量を減少させた

これにより、長期の時系列データを扱う場合、Informerを用いることで比較的少ない計算量でそれなりの精度が出せるはず

実装

下記ステップで行う

- 初期設定

- 株価データの取得

- ハイパーパラメータ設定

- 学習

- 推論

- 評価

環境:GoogleColab Pro版 GPUノーマル(device = cuda)で動確済(2023/3/26)

初期設定

必要なライブラリ、リポジトリのクローン

!pip install yfinance

!git clone https://github.com/zhouhaoyi/Informer2020.git

!ls

import os

import sys

if not 'Informer2020' in sys.path:

sys.path += ['Informer2020']

from utils.tools import dotdict

from exp.exp_informer import Exp_Informer

import torch

from torch.utils.data import DataLoader

from data.data_loader import Dataset_Pred

from torch.utils.data import DataLoader

import pandas as pd

import numpy as np

import yfinance as yf

import requests

import json

import time

株価データの取得

学習、予測を行うための株価データを取得する

Yahoo!Financeだと最短周期でも1h毎のデータしかとれないので、無料でmin単位のデータを取得できるAlpha Vantage APIを利用する

このコードでは、Appleの過去2年間のOHLCVデータを15min間隔で取得する

Alpha Vantageのサイトから無料APIを取得する(無料版は5request/min制約)

def get_stock_data(symbol, interval, api_key, slice):

url = f"https://www.alphavantage.co/query?function=TIME_SERIES_INTRADAY_EXTENDED&symbol={symbol}&interval={interval}&slice={slice}&apikey={api_key}"

response = requests.get(url)

if response.status_code == 200:

data = response.text.splitlines()

return data

else:

print(f"Error {response.status_code}: Failed to fetch data.")

return None

def convert_to_dataframe(raw_data):

header = raw_data[0].split(',')

data_rows = [row.split(',') for row in raw_data[1:]]

df = pd.DataFrame(data_rows, columns=header)

df['time'] = pd.to_datetime(df['time'])

df[['open', 'high', 'low', 'close', 'volume']] = df[['open', 'high', 'low', 'close', 'volume']].apply(pd.to_numeric)

# データフレームを古い順にソート

df.sort_values(by='time', ascending=True, inplace=True)

df.reset_index(drop=True, inplace=True)

return df

def get_full_data(symbol, interval, api_key):

# 720日間のデータを取得するためのスライスリスト

slices = [f"year1month{i}" for i in range(1, 13)] + [f"year2month{i}" for i in range(1, 13)]

all_data = []

for slice in slices:

raw_stock_data = get_stock_data(symbol, interval, api_key, slice)

if raw_stock_data:

all_data.extend(raw_stock_data[1:])

time.sleep(15) # APIの制限に従って待機(15秒)

all_data.insert(0, raw_stock_data[0])

stock_dataframe = convert_to_dataframe(all_data)

return stock_dataframe

symbol = "AAPL" #Ticker

interval = "15min" #Interval

api_key = "YOUR_API_KEY" # ここにAlpha Vantageから取得したAPIキーを入力

stock_dataframe = get_full_data(symbol, interval, api_key)

stock_dataframe.rename(columns={'time': 'date'}, inplace=True)

stock_dataframe.head()

df = stock_dataframe

output_directory = '/content/'

csv_filename = "output.csv"

output_path = os.path.join(output_directory, csv_filename)

df.to_csv(output_path, index=True)

df.head()

ハイパーパラメータ設定

close(終値)に対してOHLCVの特徴量を使って15min毎にEncodingを行い、例として3営業日後の予測を行う

この部分の条件は下記コードから抜粋

args.target = "close"

args.freq = '15m'

args.features = 'MS'

args.pred_len = 84 # =4*7*3 (15min*4=1h , 7h=1営業日の市場Open,3日)

Set train parameters

args = dotdict()

args.model = 'informer' # model of experiment, options: [informer, informerstack, informerlight(TBD)]

args.data = 'custom' # data

args.root_path = '/content/' # root path of data file

args.data_path = 'output.csv' # data file

args.features = 'MS' # forecasting task, options:[M, S, MS];

#M:multivariate predict multivariate, S:univariate predict univariate,

#MS:multivariate predict univariate

args.target = 'close' # target feature in S or MS task

args.freq = '15m' # freq for time features encoding, options:[s:secondly, t:minutely, h:hourly, d:daily, b:business days, w:weekly, m:monthly], you can also use more detailed freq like 15min or 3h

args.checkpoints = './informer_checkpoints' # location of model checkpoints

args.seq_len = 96 # input sequence length of Informer encoder

args.label_len = 48 # start token length of Informer decoder

args.pred_len = 84 # prediction sequence length

# Informer decoder input: concat[start token series(label_len), zero padding series(pred_len)]

args.enc_in = 8 # encoder input size

args.dec_in = 8 # decoder input size

args.c_out = 8 # output size

args.factor = 5 # probsparse attn factor

args.d_model = 512 # dimension of model

args.n_heads = 8 # num of heads

args.e_layers = 2 # num of encoder layers

args.d_layers = 1 # num of decoder layers

args.d_ff = 2048 # dimension of fcn in model

args.dropout = 0.05 # dropout

args.attn = 'prob' # attention used in encoder, options:[prob, full]

args.embed = 'timeF' # time features encoding, options:[timeF, fixed, learned]

args.activation = 'gelu' # activation

args.distil = True # whether to use distilling in encoder

args.output_attention = False # whether to output attention in ecoder

args.mix = True

args.padding = 0

args.freq = 'h'

args.batch_size = 32

args.learning_rate = 0.0001

args.loss = 'mse'

args.lradj = 'type1'

args.use_amp = False # whether to use automatic mixed precision training

args.num_workers = 0

args.itr = 1

args.train_epochs = 20

args.patience = 3

args.des = 'exp'

args.use_gpu = True if torch.cuda.is_available() else False

args.gpu = 0

args.use_multi_gpu = False

args.devices = '0,1,2,3'

GPUの設定

args.use_gpu = True if torch.cuda.is_available() and args.use_gpu else False

if args.use_gpu and args.use_multi_gpu:

args.devices = args.devices.replace(' ','')

device_ids = args.devices.split(',')

args.device_ids = [int(id_) for id_ in device_ids]

args.gpu = args.device_ids[0]

# Set augments by using data name

data_parser = {

'custom':{'data':'output.csv','T':'close','M':[6,6,6],'S':[1,1,1],'MS':[6,6,1]}, #特徴量の数に応じてここの配列を変更する

}

if args.data in data_parser.keys():

data_info = data_parser[args.data]

args.data_path = data_info['data']

args.target = data_info['T']

args.enc_in, args.dec_in, args.c_out = data_info[args.features]

args.detail_freq = args.freq

args.freq = args.freq[-1:]

Exp = Exp_Informer

print('Args in experiment:')

print(args)

学習

for ii in range(args.itr):

# setting record of experiments

setting = '{}_{}_ft{}_sl{}_ll{}_pl{}_dm{}_nh{}_el{}_dl{}_df{}_at{}_fc{}_eb{}_dt{}_mx{}_{}_{}'.format(args.model, args.data, args.features,

args.seq_len, args.label_len, args.pred_len,

args.d_model, args.n_heads, args.e_layers, args.d_layers, args.d_ff, args.attn, args.factor, args.embed, args.distil, args.mix, args.des, ii)

# set experiments

exp = Exp(args)

# train

print('>>>>>>>start training : {}>>>>>>>>>>>>>>>>>>>>>>>>>>'.format(setting))

exp.train(setting)

# test

print('>>>>>>>testing : {}<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<'.format(setting))

exp.test(setting)

torch.cuda.empty_cache()

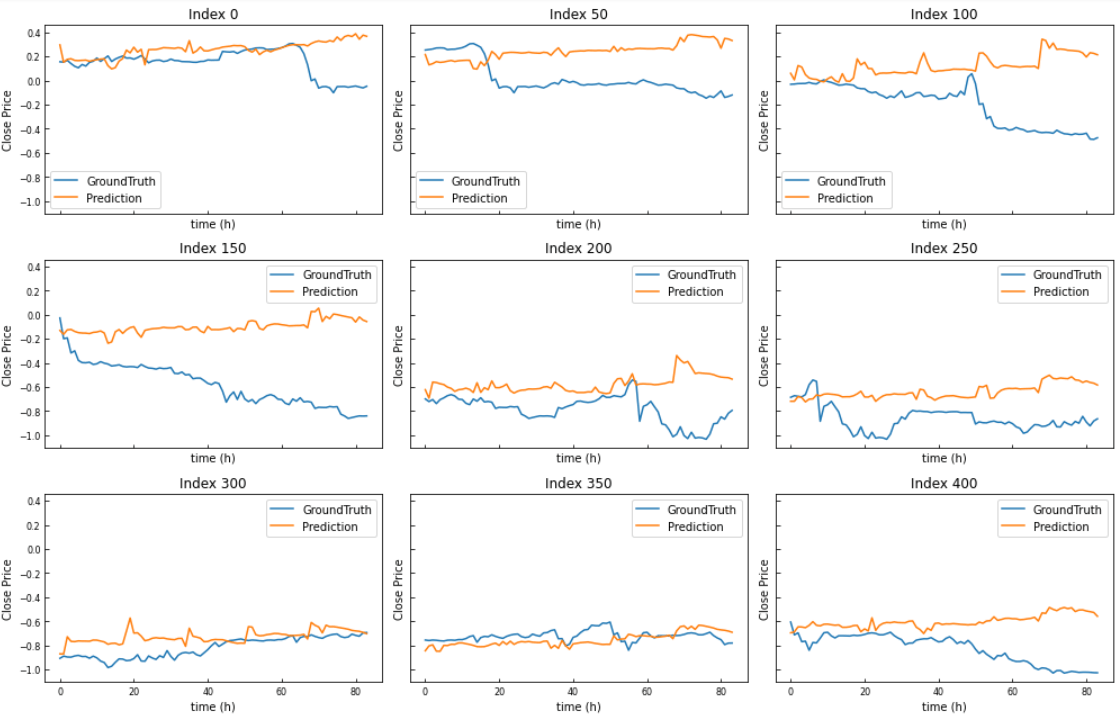

mse:0.042731158435344696, mae:0.15262167155742645となった

推論

# set saved model path

setting = 'informer_custom_ftMS_sl96_ll48_pl84_dm512_nh8_el2_dl1_df2048_atprob_fc5_ebtimeF_dtTrue_mxTrue_exp_0'

# path = os.path.join(args.checkpoints,setting,'checkpoint.pth')

# If you already have a trained model, you can set the arguments and model path, then initialize a Experiment and use it to predict

# Prediction is a sequence which is adjacent to the last date of the data, and does not exist in the data

# If you want to get more information about prediction, you can refer to code `exp/exp_informer.py function predict()` and `data/data_loader.py class Dataset_Pred`

exp = Exp(args)

exp.predict(setting, True)

prediction = np.load('./results/'+setting+'/real_prediction.npy')

prediction.shape

Data = Dataset_Pred

timeenc = 0 if args.embed!='timeF' else 1

flag = 'pred'; shuffle_flag = False; drop_last = False; batch_size = 1

freq = args.detail_freq

data_set = Data(

root_path=args.root_path,

data_path=args.data_path,

flag=flag,

size=[args.seq_len, args.label_len, args.pred_len],

features=args.features,

target=args.target,

timeenc=timeenc,

freq=freq

)

data_loader = DataLoader(

data_set,

batch_size=batch_size,

shuffle=shuffle_flag,

num_workers=args.num_workers,

drop_last=drop_last)

len(data_set), len(data_loader)

評価、可視化

# When we finished exp.train(setting) and exp.test(setting), we will get a trained model and the results of test experiment

# The results of test experiment will be saved in ./results/{setting}/pred.npy (prediction of test dataset) and ./results/{setting}/true.npy (groundtruth of test dataset)

preds = np.load('./results/'+setting+'/pred.npy')

trues = np.load('./results/'+setting+'/true.npy')

# [samples, pred_len, dimensions]

preds.shape, trues.shape

import matplotlib.pyplot as plt

def plot_predictions(trues, preds, start_index, step, num_plots):

num_rows = num_plots // 3

num_cols = 3

fig, axes = plt.subplots(num_rows, num_cols, figsize=(14, 3 * num_rows), sharex=True, sharey=True)

for i, ax in enumerate(axes.flatten()):

if i < num_plots:

index = start_index + i * step

ax.plot(trues[index, :, -1], label='GroundTruth')

ax.plot(preds[index, :, -1], label='Prediction')

ax.set_title(f'Index {index}')

ax.legend()

ax.set_xlabel('time (h)')

ax.set_ylabel('Close Price')

ax.tick_params(axis='both', which='both', labelsize=8, direction='in')

else:

ax.axis('off')

# グラフを表示

plt.tight_layout()

plt.show()

plot_predictions(trues, preds, start_index=0, step=50, num_plots=9)

横軸が84じゃなくてmax21hですね。(15min×84)

終わり

Discussion