📝

FXデータ分析:ロンドンフィックスのGBPUSDを可視化する

プロンプト1

ロンドンフィックスを計算します。

夏時間は、毎年3月の最終日曜日1時(UTC時間)から10月最終日曜日1時までです。

プロンプト2

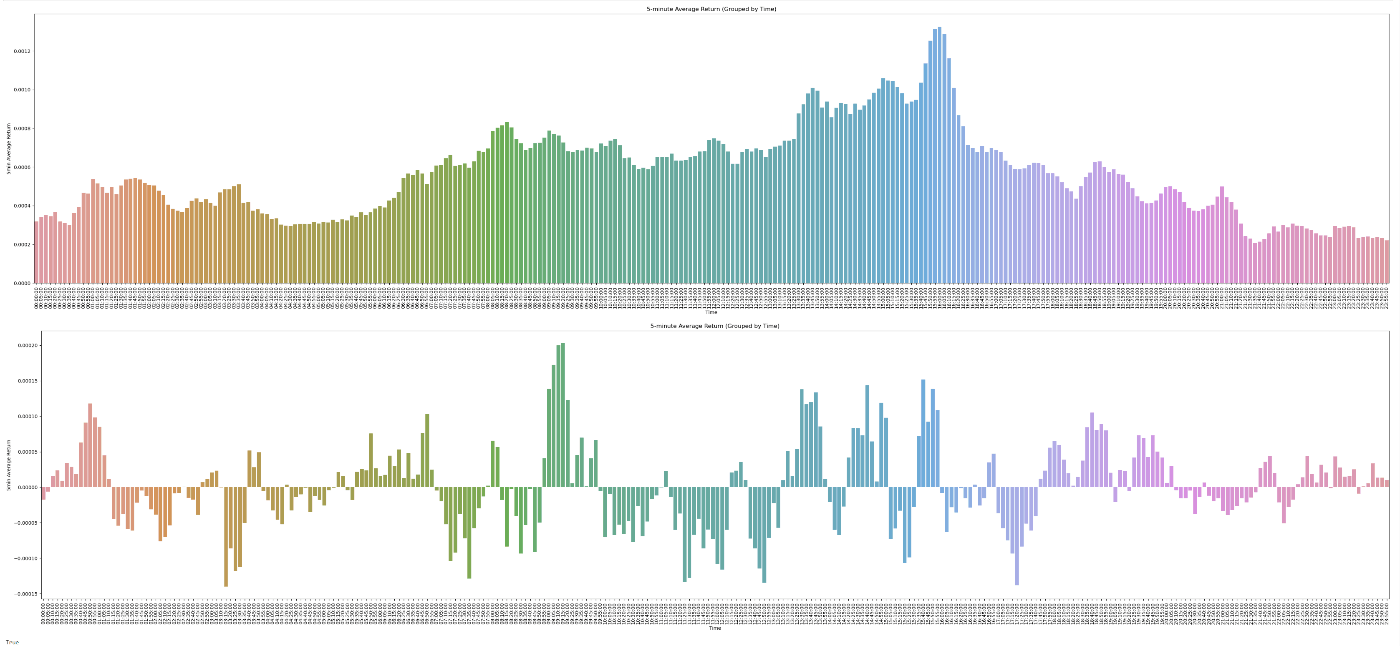

このコードは値動きの特徴を可視化するものです。

現在のGMT+9を使っています。夏時間は夏時間で集計して、冬時間は冬時間で集計してください。

プロンプト3

すべてロンドンの時間基準にしてください。

import pandas as pd

import MetaTrader5 as mt5

from datetime import timedelta

import seaborn as sns

import matplotlib.pyplot as plt

from datetime import datetime

from pandas.tseries.holiday import AbstractHolidayCalendar, Holiday, nearest_workday, MO

from pandas.tseries.offsets import DateOffset, Day

# MT5への接続

if not mt5.initialize():

print("initialize() failed, error code =",mt5.last_error())

quit()

def high_low_ratio(df):

return (df['high'] - df['low']) / df['low']

def close_open_ratio(df):

return (df['close'] - df['open']) / df['open']

class BSTCalendar(AbstractHolidayCalendar):

rules = [

Holiday('BST Start', month=3, day=31, offset=DateOffset(weekday=MO(-1))),

Holiday('BST End', month=10, day=31, offset=DateOffset(weekday=MO(-1))),

]

def bst_dates(year):

inst = BSTCalendar()

return inst.holidays(datetime(year-1, 12, 31), datetime(year, 12, 31))

def fetch_and_prepare(symbol, timeframe, count, ratio_calculation, column_name):

# データの取得

rates = mt5.copy_rates_from_pos(symbol, timeframe, 0, count)

# DataFrameに変換

df = pd.DataFrame(rates)

# 日時をPandasの日時形式に変換

df['time'] = pd.to_datetime(df['time'], unit='s')

# BSTの開始日と終了日を取得

year = df['time'].dt.year[0] # 始点の年を取得

bst_start, bst_end = bst_dates(year)

# BSTとGMTの適用

df.loc[df['time'].between(bst_start, bst_end), 'time'] += timedelta(hours=1)

df.loc[~df['time'].between(bst_start, bst_end), 'time'] += timedelta(hours=0)

df[column_name] = ratio_calculation(df)

return df

def plot_avg_return(df, column_name):

# インデックスを日付に変換

df.set_index('time', inplace=True)

# 5分ごとの平均リターンを計算

df['5min_avg_return'] = df[column_name].rolling(window=5).mean()

# 時刻をグループ化して平均を計算

grouped_df = df.groupby(df.index.time).mean()

# 時刻を文字列に変換

grouped_df.index = grouped_df.index.astype(str)

# グラフの作成

plt.figure(figsize=(50, 10))

sns.barplot(x=grouped_df.index, y=grouped_df['5min_avg_return'])

plt.xlabel('Time')

plt.ylabel('5min Average Return')

plt.title('5-minute Average Return (Grouped by Time)')

# X軸のラベルを斜めに表示

plt.xticks(rotation=90)

plt.show()

# 読み込む通貨ペアと時間枠、データの件数を指定

symbol = 'GBPUSDm'

timeframe = mt5.TIMEFRAME_M5

count = 100000

df = fetch_and_prepare(symbol, timeframe, count, high_low_ratio, 'high_low_ratio')

plot_avg_return(df, 'high_low_ratio')

df = fetch_and_prepare(symbol, timeframe, count, close_open_ratio, 'close_open_ratio')

plot_avg_return(df, 'close_open_ratio')

mt5.shutdown()

プロンプト4

月末だけにしてください。

import pandas as pd

import MetaTrader5 as mt5

from datetime import timedelta

import seaborn as sns

import matplotlib.pyplot as plt

from datetime import datetime

from pandas.tseries.holiday import AbstractHolidayCalendar, Holiday, nearest_workday, MO

from pandas.tseries.offsets import DateOffset, Day

# MT5への接続

if not mt5.initialize():

print("initialize() failed, error code =",mt5.last_error())

quit()

def high_low_ratio(df):

return (df['high'] - df['low']) / df['low']

def close_open_ratio(df):

return (df['close'] - df['open']) / df['open']

class BSTCalendar(AbstractHolidayCalendar):

rules = [

Holiday('BST Start', month=3, day=31, offset=DateOffset(weekday=MO(-1))),

Holiday('BST End', month=10, day=31, offset=DateOffset(weekday=MO(-1))),

]

def bst_dates(year):

inst = BSTCalendar()

return inst.holidays(datetime(year-1, 12, 31), datetime(year, 12, 31))

def fetch_and_prepare(symbol, timeframe, count, ratio_calculation, column_name):

# データの取得

rates = mt5.copy_rates_from_pos(symbol, timeframe, 0, count)

# DataFrameに変換

df = pd.DataFrame(rates)

# 日時をPandasの日時形式に変換

df['time'] = pd.to_datetime(df['time'], unit='s')

# BSTの開始日と終了日を取得

year = df['time'].dt.year[0] # 始点の年を取得

bst_start, bst_end = bst_dates(year)

# BSTとGMTの適用

df.loc[df['time'].between(bst_start, bst_end), 'time'] += timedelta(hours=1)

df.loc[~df['time'].between(bst_start, bst_end), 'time'] += timedelta(hours=0)

# 月末のデータのみ抽出

df = df[df['time'].dt.is_month_end]

df[column_name] = ratio_calculation(df)

return df

def plot_avg_return(df, column_name):

# インデックスを日付に変換

df.set_index('time', inplace=True)

# 5分ごとの平均リターンを計算

df['5min_avg_return'] = df[column_name].rolling(window=5).mean()

# 時刻をグループ化して平均を計算

grouped_df = df.groupby(df.index.time).mean()

# 時刻を文字列に変換

grouped_df.index = grouped_df.index.astype(str)

# グラフの作成

plt.figure(figsize=(50, 10))

sns.barplot(x=grouped_df.index, y=grouped_df['5min_avg_return'])

plt.xlabel('Time')

plt.ylabel('5min Average Return')

plt.title('5-minute Average Return (Grouped by Time)')

# X軸のラベルを斜めに表示

plt.xticks(rotation=90)

plt.show()

# 読み込む通貨ペアと時間枠、データの件数を指定

symbol = 'GBPUSDm'

timeframe = mt5.TIMEFRAME_M5

count = 100000

df = fetch_and_prepare(symbol, timeframe, count, high_low_ratio, 'high_low_ratio')

plot_avg_return(df, 'high_low_ratio')

df = fetch_and_prepare(symbol, timeframe, count, close_open_ratio, 'close_open_ratio')

plot_avg_return(df, 'close_open_ratio')

mt5.shutdown()

Discussion